The first half of 2023 has been an unexpected rollercoaster ride for the global financial markets. After a tumultuous 2022, marked by significant losses across asset classes, inflation spikes, and rapid rate hikes, investors entered the new year with a cautious outlook. However, the markets have defied expectations, showcasing resilience and delivering impressive returns in the face of challenges.

In this market review, we explore:

- Surprising H12023 growth

- Dominance of mega-cap tech stocks

- The case of disinflation

- Fed’s last rate hike and prospects of soft landing

- Investment outlook for H22023

Markets Defy Expectations in H1 2023

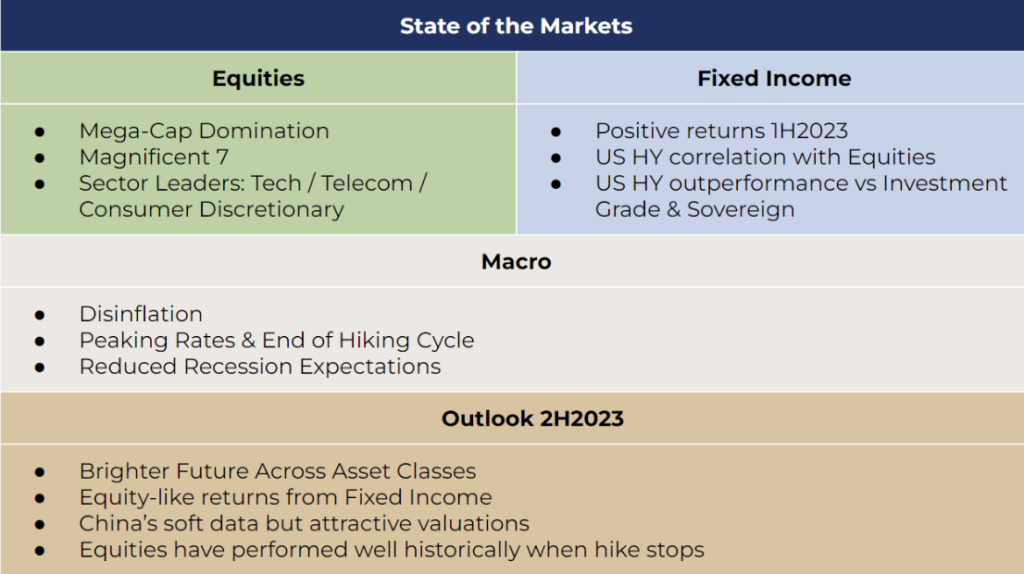

Despite pessimistic forecasts, the equity markets have shown remarkable strength in H1 2023. NASDAQ and the technology sector have led the rally for the year. US Stocks outperformed global stocks with S&P 500 surging 16.4% while MSCI World rising by 14.1%. A notable outlier was China with the benchmark index giving up all of its returns as expectations of a post reopening surge were dwarfed with persistent worries over growth and geopolitics.

Sector and Asset-Class Performance Dispersed

While tech-related stocks shone brightly, defensive sectors such as utilities, healthcare, and consumer staples struggled to keep pace. Financials initially benefited from rising rates but faced headwinds due to the regional bank crisis in the US. Additionally, energy stocks suffered due to a significant drop in oil prices.

Fixed income faced significant volatility throughout these six months, as cracks started to form from the effects of this accelerated cycle of monetary tightening. High Yield beat Investment Grade/Sovereign even as interest rates were volatile during this period, with expected peak Fed rate constantly being repriced, debt ceiling brinkmanship and fears of contagion in the banking sector. High Yield correlated more with equities, gaining an edge over the other fixed income sub sectors.

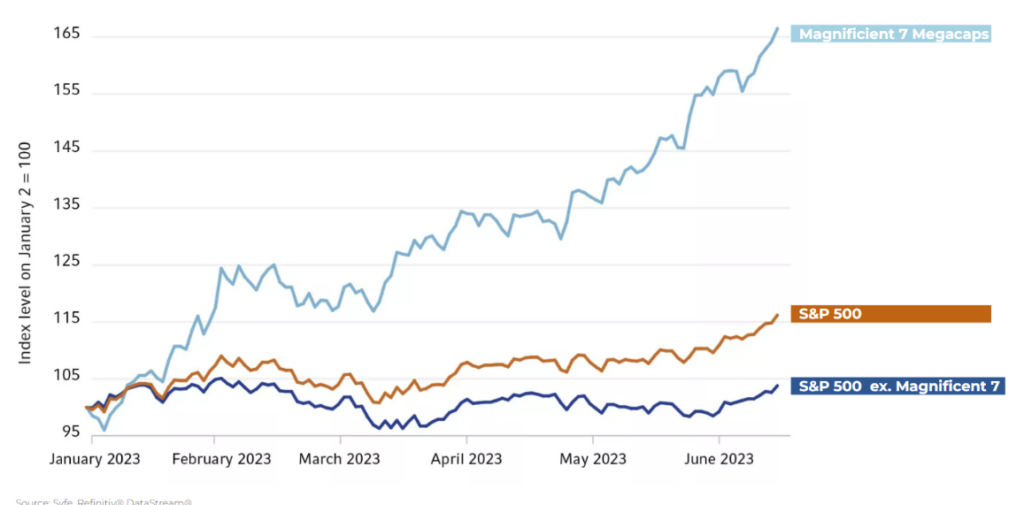

Mega-caps Dominated Equity Market Returns Magnified by the AI Hype

At the forefront of the market’s surge were a select group of mega-cap technology stocks – Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, and Tesla. These companies, referred to as the ‘Magnificent 7’, form a significant part of S&P 500 and accounted for an astounding 73% of the index gains, propelling it towards bull market territory.

Interest in AI has swelled this year since the launch of ChatGPT – an AI-powered conversational agent. This has generated a lot of excitement and frenzy among investors looking for new growth drivers to the economy. The optimism has centered around productivity boost through AI and its transformational impact across a wide range of industries.

However, S&P 500 returns, excluding the Magnificent 7, were relatively subdued with less than 5% gains for the first half of 2023. Moving ahead, whether the rally becomes more broad based or fades away will depend on how much of the hype around AI translates into concrete outcomes.

The Case for Disinflation

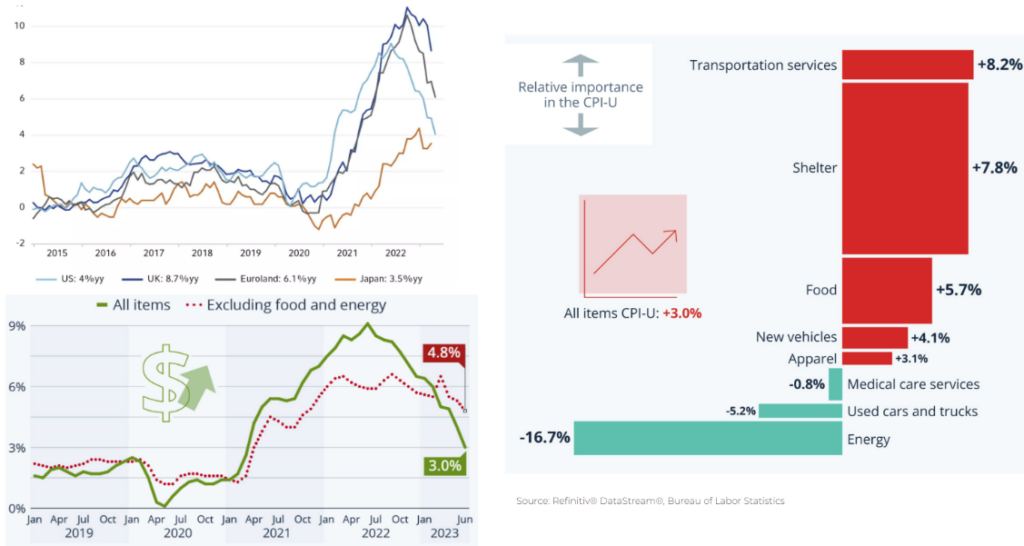

Headline inflation has peaked in most regions and is now firmly in a downward trajectory, driven by factors such as lower energy prices and fewer supply chain disruptions.

The US has led the inflation rates lower as the CPI grew by only 3% p.a. in June, down from 4% a month earlier and marking its smallest rise since 2021. Core inflation, which excludes food and energy, is proving stickier, but it has begun to turn lower. It increased 4.8% p.a. in June – again the lowest rate since 2021.

Notably, the shelter subindex, representing rent and utility payments, played a substantial role in June’s inflation increase, accounting for over 70% of the overall CPI rise. Excluding shelter, prices would have increased by just 0.7 percent year-over-year basis.

So why should we expect lower core inflation going forward?

- Energy prices continue to cool even with supply controls being put in place.

- Shelter inflation is expected to decline. Market analysis shows that at least half of the post-covid premium on new rental units has unwound – which will reduce upward pressure on rental renewals.

- There is also significant progress on the labor market with the sequential growth in average hourly earnings having already slowed to 4%.

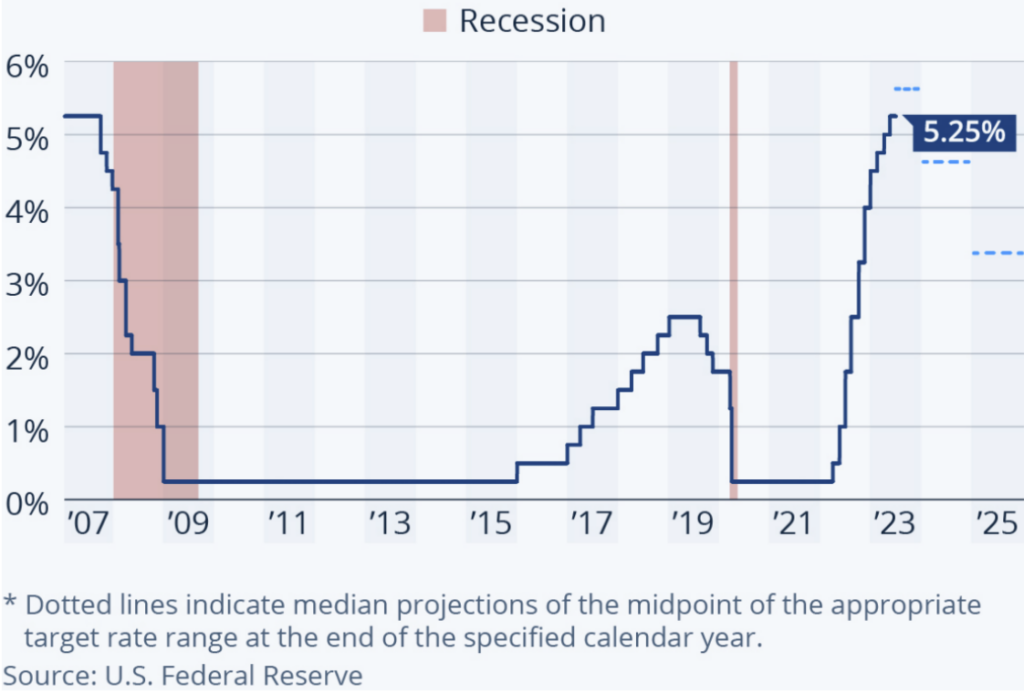

25 Bps Last Hike of the Cycle?

The Federal Reserve, on a rate-hiking spree since March 2022, raised its benchmark rate by another 25 basis points during its July meeting after a pause in June, bringing it to the 5.25%-5.50% range.

Looking ahead, while the FED dot plot shows possibility for more rate hikes, data suggests that inflation will likely moderate more swiftly than what the FED currently projects. This might lead to the July rate hike being the last one for the current cycle. However, the prospects of a rate cut moves further down the road into 2024 as the FED will remain cautious in its quest to achieve the 2% inflation rate target.

Soft Landing on the Horizon?

Easing inflation, a labor market that remains strong and economic resilience have made the market much more optimistic about the economic outlook.

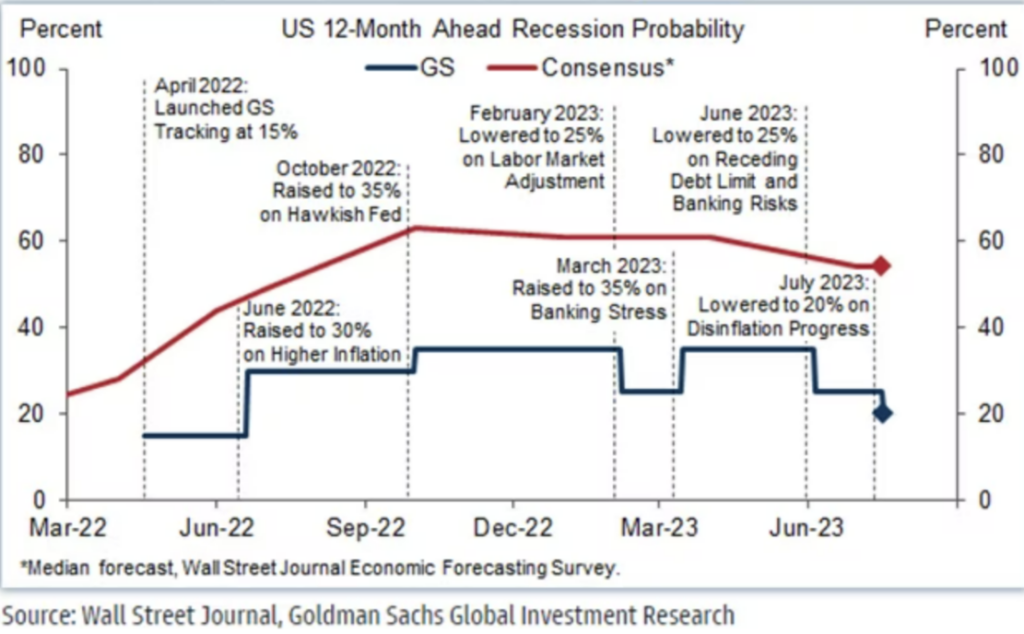

Surveys conducted by The Wall Street Journal reveal that the probability of a recession in the next 12 months has decreased to 54%, down from 61% in previous assessments. Goldman Sachs, came out with even more optimistic views, lowering the recession probability from 25% to 20%, on the back of the ongoing positive economic activity.

Amidst hopes of a smoother and more sustainable economic trajectory, the pathway to achieve a “soft landing” is back on the table!

- US economic activity remains resilient, with Q2 GDP growth tracking 2.3%.

- Consumer sentiment rebounded sharply from depressed levels.

- Unemployment levels fell back to 3.5% in June, and initial jobless claims reversed their most recent mini-spike.

- Inflationary pressures are easing and there are strong reasons to expect ongoing disinflation.

- The yield curve remains inverted but with expectations of FED stopping rate hikes after the July cycle, the pessimism baked in the yield curve will likely ease.

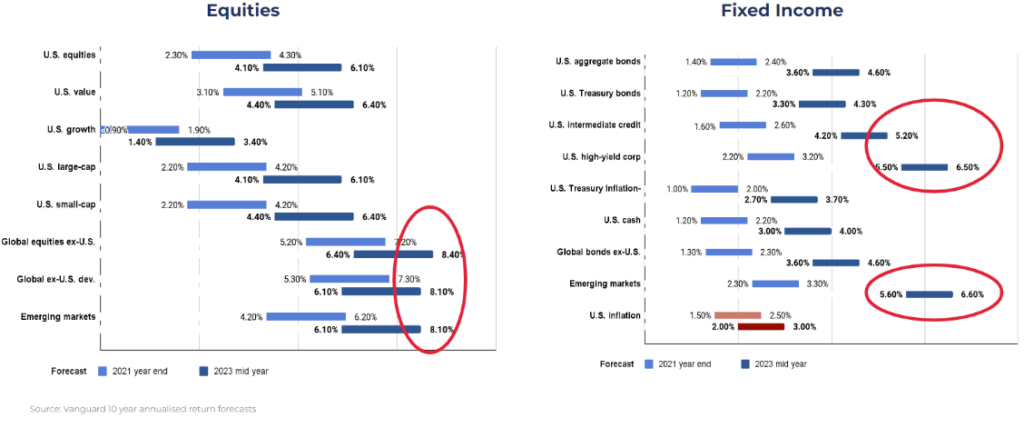

A Brighter Future Across Asset Classes

Many investors have fled to cash as interest rates soared over the last one year. However, coming to the second half of the year, long-term capital markets returns show a more appealing investment environment. Across equity and fixed income, the expected returns in the next 10 years have shifted meaningfully to the right compared to 2021.

On the equity side, while the valuations look rich in the US, there is growing optimism around non-US equities, which should be propelled by a combination of higher dividend yields, multiple expansion and a weaker dollar.

On fixed income, US fixed income returns should improve as they start from a much higher yield point and benefit from price appreciation and declining yields. From a total return perspective, emerging markets debt looks attractive.

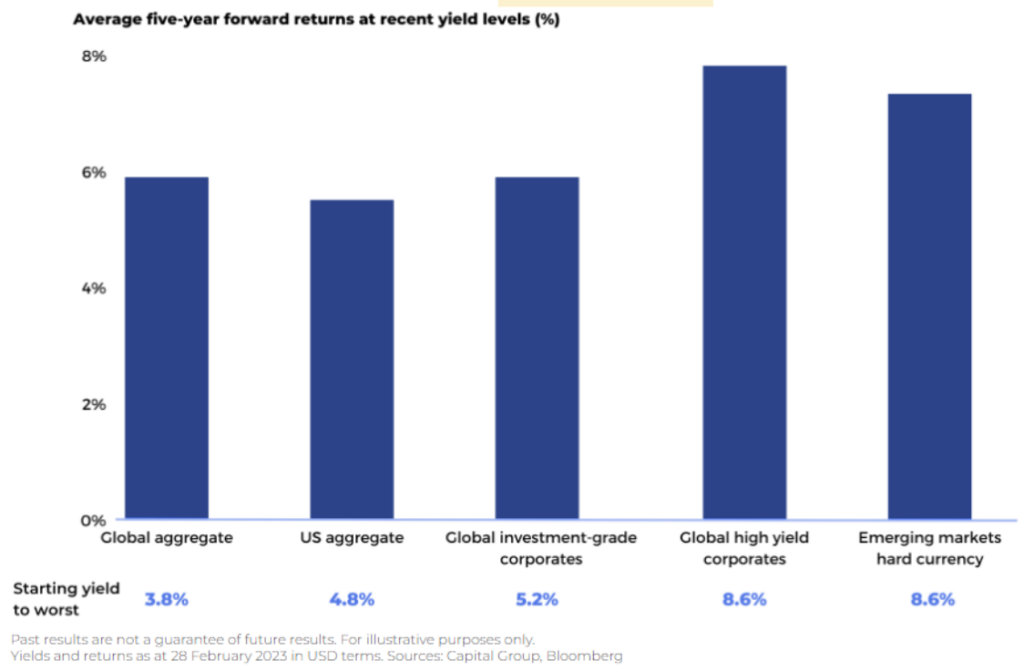

Fixed Income Offers Compelling Opportunities

Current yields are at some of their highest levels across different fixed income sectors, meaning that fixed income now offers meaningful income, yield protection and potential for capital appreciation. Investment-grade corporate credit currently yields north of 5%, presenting an attractive option for those seeking stable returns with lower volatility and downside risk.

Also, historically, when yield levels reach the point where we are at, it has given attractive returns in a 5-year period going forward. At this point, the bond market offers potential for equity-like returns with much less volatility and downside risk, making it valuable for building resilient portfolios.

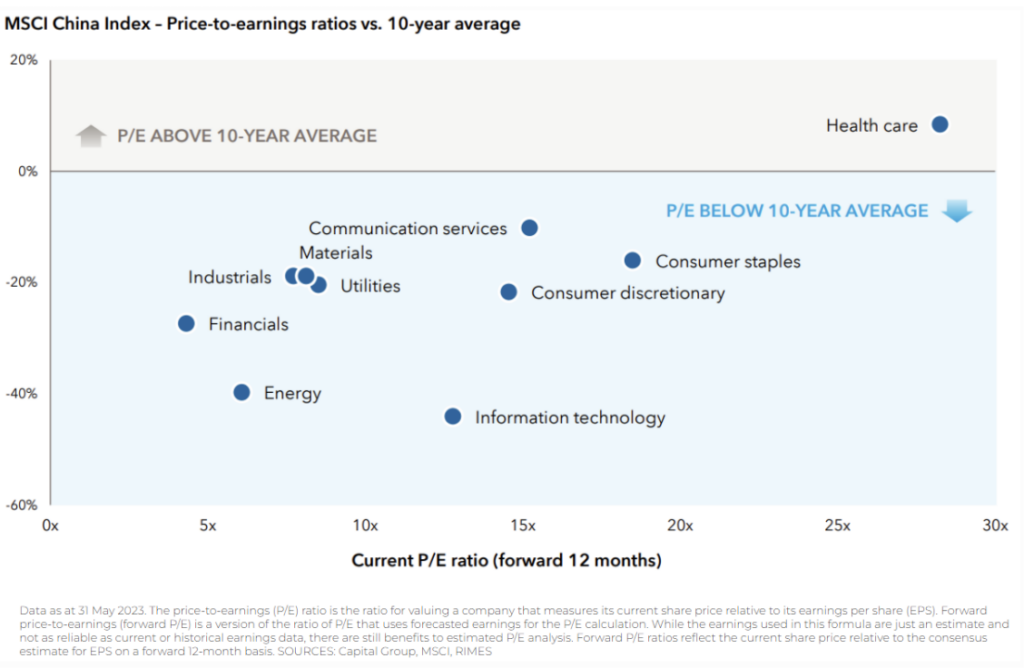

China’s Soft Data but Attractive Valuations

China’s second-quarter GDP print missed expectations as it grew by 6.3% vs forecasts of 7.3%. It marked a 0.8% quarter over quarter growth, which is much slower than the 2.2% quarterly growth recorded in the first three months of the year. Another key concerning stat was the unemployment rate among young people aged 16 to 24 hitting a new record high of 21.3% in June.

Quarterly growth numbers in China are expected to rebound moving forward as some negative factors fade in Q3 and policy continues to ease. Despite weaker growth and continued structural concerns, Chinese equities remain attractively priced compared to their long-term averages, with a pro-growth policy/regulatory backdrop.

The country’s transformation from an “old economy” to a “new economy,” driven by technological innovation, service-oriented industries, and the rising power of Chinese consumers, provides a compelling case for investors to keep a close eye on China’s future developments.

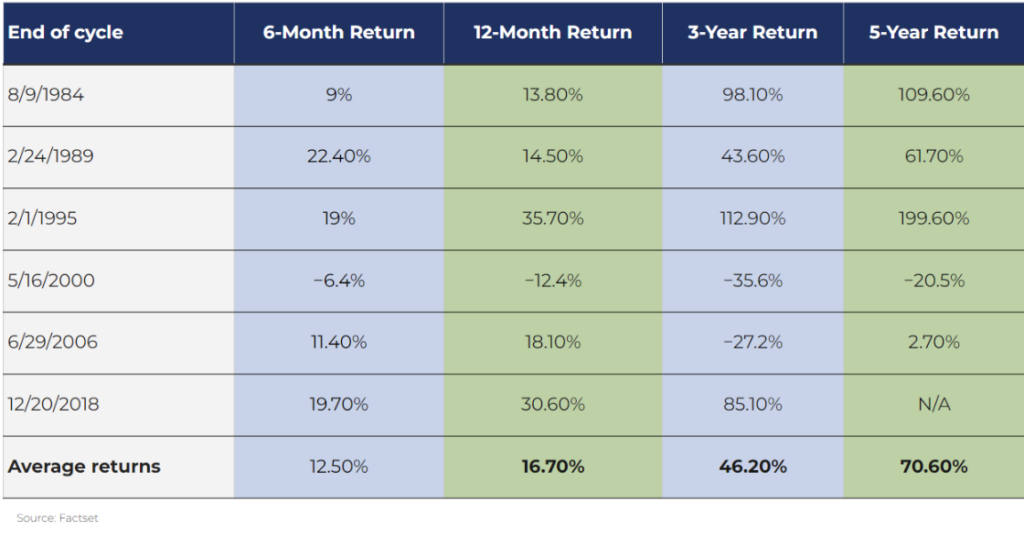

Historical Returns in Equity Markets Post-Rate Hikes

The S&P 500 has shown remarkable performance, up more than 15% year-to-date and over 25% since last fall. The index now trades at a roughly 25 P/E ratio, which is much higher than the historical average of 16. While many predict a flat to negative return for the next 12 months, history indicates that the index has continued to surge after previous Fed tightening cycles concluded.

The S&P 500 gained 16.7% on average in the 12 months following the prior six conclusions to Fed tightening cycles – far outperforming the index’s historic 12% annual return. Even on a three year forward basis, it has grown by an average of 46.2% after the conclusion of its prior six hiking cycles.

SUMMARY

The first half of 2023 brought unexpected twists and turns to the market, challenging prior expectations. What began with apprehension and uncertainty gradually morphed into a story of resilience, surprising growth, and newfound optimism. Mega-cap tech stocks and the rising interest in AI have been at the forefront of this resilience.

As we head into the second half of the year, opportunities across various asset classes emerge, providing investors with compelling prospects for growth and income diversification. As the markets continue to evolve, embracing change and staying agile will be key to unlocking the full potential of growth in 2023 and beyond.

You must be logged in to post a comment.