Gearing up for hikes

The Federal Reserve’s rate setting committee (FOMC) is set to meet next week (July 26-27). The market is expecting a 75bps hike (similar to the one delivered in June) to combat inflation, which rose to 9.1%.

Following the July meeting, economists see a smaller move in September. The committee is up against a tough fight – trying to bring inflation down without tipping the economy into a prolonged recession.

Running up that hill (too)

Like the Fed, the European Central Bank (ECB) made an outsized move this week – raising interest rates by double the amount that was expected from forward guidance. The somewhat unexpected move came as officials stated that they have to ensure that inflation expectations do not become entrenched, leading to potential wage price spirals and making it much harder to tame inflation.

Interestingly, the ECB has reversed hikes in 2008 and 2011 due to the Global Financial Crisis (GFC) and European Debt Crisis. Both times, interest rates were raised in July and subsequently reversed a few months later.

Again, there is merit in making a bigger move now, in case growth slows even more in the coming months. With inflation in the high single digits and bond yields being positive (after years of negative yielding debt), the ECB has some way to go in raising rates, starting effectively from zero.

Anchored at 3%

Despite high inflation and big hikes coming, yields on the 10 year US Treasury remain anchored at about 3%. As short term yields go above longer term yields, we get a treasury curve inversion (typically, investors look at the yield on the 2 year treasury vs that of the ten year).

A yield curve inversion has preceded every US recession in the last 50 years. This is seen as a recession signal, but the economist, Campbell Harvey, who is seen as a voice of authority on yield curve inversions prefers to use the 3 month Treasury instead of the 2 year, as it is more representative of current market conditions. Currently, 3 month yields remain below 10 year yields, but the gap has been narrowing as 3 month yields go up while 10 year yields remain at about 3%.

Many bond market participants think that the Fed is going to have to raise interest rates a bit too much and tip the economy into a recession, even if it will be a mild one. In this case, treasury yields will remain range bound. So, investors are still buying long dated treasury bonds now (when yields are high enough), locking that in even if yields could go higher as the Fed raises interest rates.

Technologies on Spotlights

US listed Chinese stocks rose, helped by a media report that Beijing is researching a tiered-data strategy to prevent firms from US delistings, although regulators denied.

China fined Didi Global more than 8bn RMB (1.2bn USD), marking the end of a one year investigation. Market do speculate that once the investigation is over, Didi App could be relisted on the domestic App Store again. Didi is expected to prepare for the HK listing in H2.

Alibaba Group said it will apply for a primary listing in Hong Kong, a move that could make itself accessible by mainland Chinese investors through the stock connect program.

Real estate rebounded fiercely on these two days after sharp drops on delinquent mortgage worry. Chinese policymakers are planning a rescue fund of RMB 200-300 billion. This rescue fund supports 12 developers and a few new distressed real estate firms nominated by local authorities. July 60-city weekly sales were mostly flat week on week, with year on year decline narrowing from 40% to 32%. Since there may be delays in sales filing, to assess the impact on homebuyers’ confidence after the mortgage suspension noises, we think the next 1-2 weeks will be key. Market is still seeing if this can fully ease the core concern of low homebuyers’ confidence.

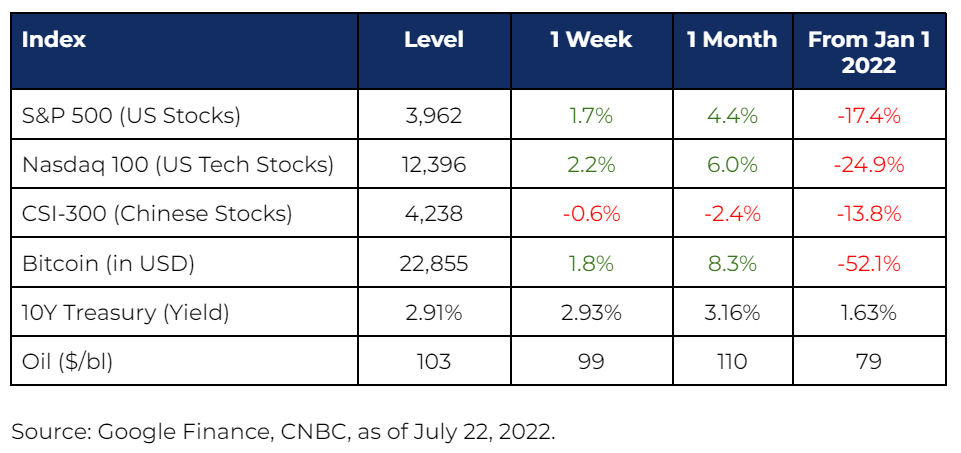

Market Stats