Inflation peaks again

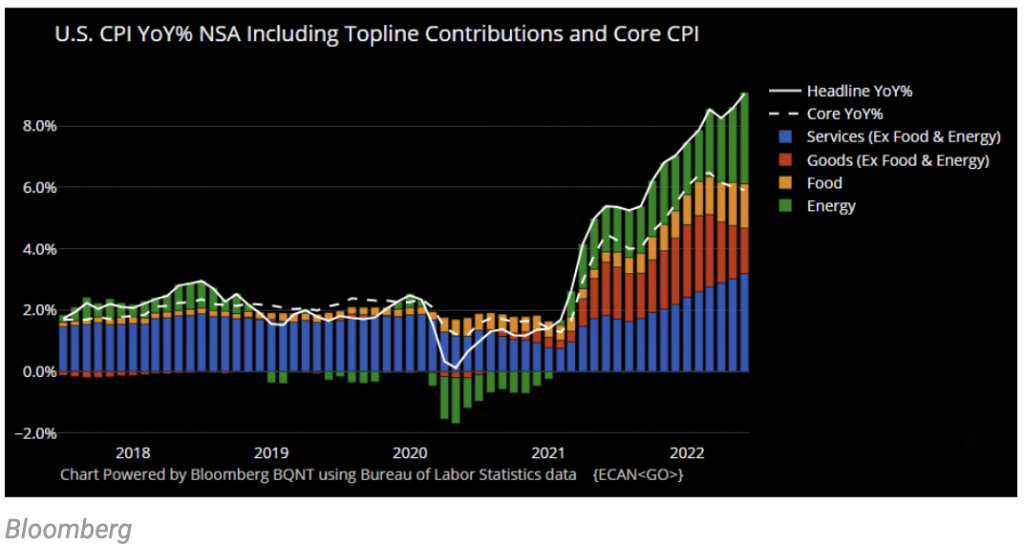

Inflation in the US surged (again!) to 9.1% in June, marking a new high in 40 years. No one was expecting a low figure, but this surprised on the upside. A rapid re-pricing of Fed expectations followed and researchers from Citi gained attention for putting a 1.00% hike on the table, but qualified that the Fed would have to be nimble and to be prepared to cut rates if needed too.

The next FOMC meeting happens in two weeks (July 26-27). We will be tracking what Federal Reserve officials say in interviews next week before they enter a quiet period a week prior to FOMC meetings. So far, based on public comments from Fed staff, a 75bps increase at the July meeting would be the base case.

Looking at the breakdown of components that go into CPI, prices of food and goods (yellow and red bars) continue to moderate but energy surged. Post the CPI-print, several economists pointed out that oil prices have started to moderate in the middle of June, and based on futures prices are likely to remain range round, possibly signalling that inflation may have peaked as long as energy prices remain range bound. This has been a familiar tune and many don’t quite know what to make of it!

All over the place

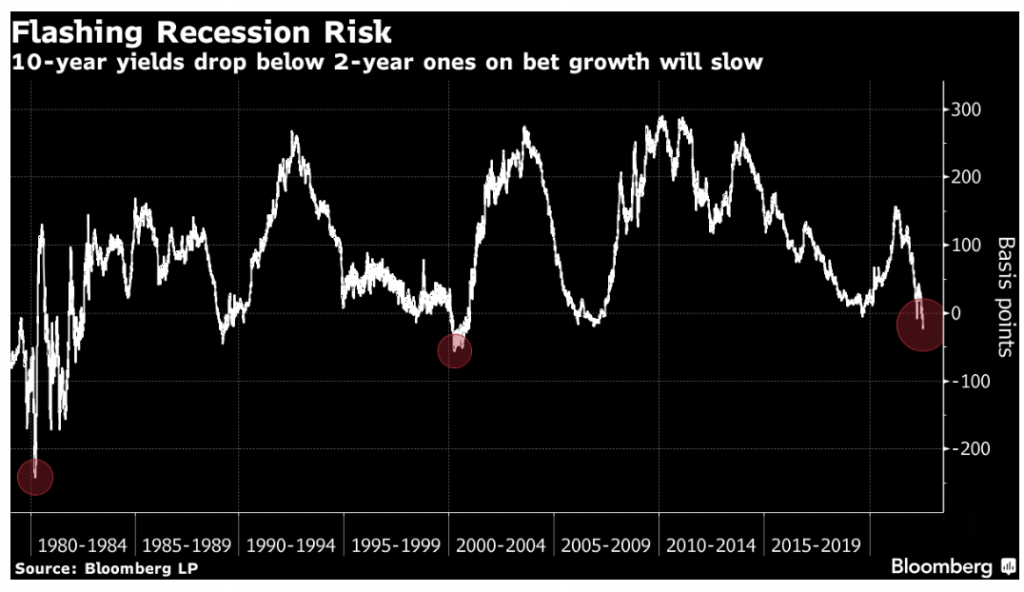

Post the inflation print, Treasury curve inversion (the yield on the 2 year treasury being above that of the ten year, showing negative term premium) deepened. 10 year treasury yields fell 28bps below that of 2 year bonds, the most since 2000. This suggests that many bond market participants think that the Fed is going to raise interest rates a bit too much and tip the economy into a recession, even if it will be a mild one.

China’s growth slows

The market weakened significantly last week, and only the ChiNext Index remained relatively stronger.

Last Friday China GDP grew only 0.4% in the second quarter. A low figure was expected and the market consensus at 1.0% accounted for that. The low GDP growth figure is part of growing evidence that the target of 5.5% may seem increasingly challenging.

The spreading unfinished residential projects and relevant delinquent mortgages unsettled the market. This time, the problem is more relevant to the homebuyers’ confidence and people have been expecting acute and decisive interventions by the government to stop the whole spiral. ness has spread to the level of confidence, so it is necessary to observe whether the government has emergency intervention policies this month.

For all the big 4 SOE banks, the capital reserve ratio ranges from 16-18% and the regulated requirement is 8.5%. There should be enough buffer for the relevant mortgages. SOE bank typical loan books consist of ⅓ mortgages and the existing delinquent mortgages account for less than 1% of the non-performing loan.

Construction for new buildings have stalled in several cities and reports of households holding back on their mortgage payments rattled banks this week. In June, Chinese home prices continued to fall for the tenth consecutive month.

We should pay attention to monthly contract sales for the remainder of H2. If June contract sales momentum can last for the rest of the year, it would at least rescue the major property developers from ICU.

As we mentioned two weeks ago, there are more insider sales among the Technology and Innovation sectors. BYD was a new relevant suspect. 225m BYD shares registered with CitiGroup on the Hong Kong stock market’s CCASS on last Monday Jul 12. This matched the size of the stake in BYD’s Hong Kong stock held by Berkshire Hathaway. Market speculates that Warren Buffett has an upcoming plan to exit this BYD investment. Berkshire bought 225 million shares in BYD in September 2008 for HK$8 per share and the return has been over 2,000%.

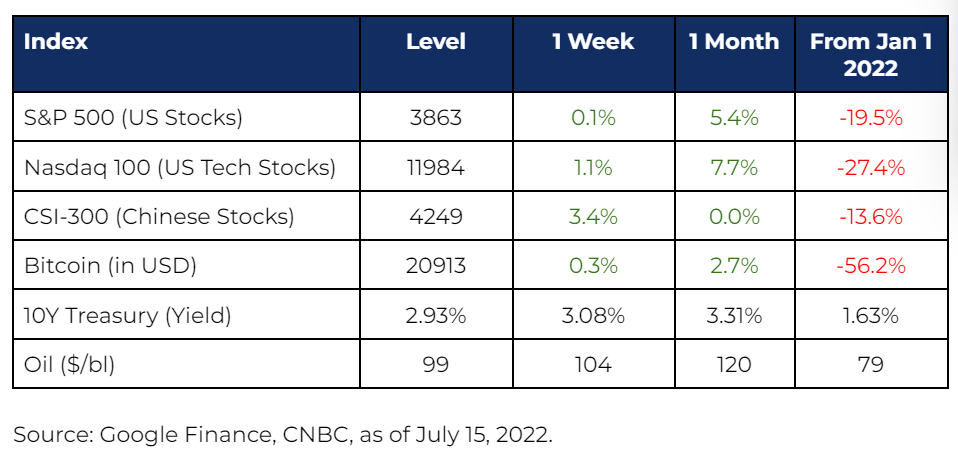

Market Stats